Home / Forex news / OIL MARKET WEEK AHEAD: Worse Before it Gets Better

The week ahead in Europe will get worse before it gets better, bringing a large level of uncertainty to the oil markets.

The number of new coronavirus cases in Germany and France is gathering critical mass, big enough to start disrupting working life, close schools and bring businesses to a standstill. Looking at how Italy has responded to the spread there, European countries are looking at school and university closures, travel restrictions and the cancellation of events that bring a large number of people into close proximity. The European Commission has already started teleconferencing instead of meeting in person after the first cases of the virus were registered in Brussels.

The UK is lagging “behind” this curve with some 160 registered cases versus Germany’s and France’s 570. For the oil markets this will mean reduced transport demand and to a lesser extent industrial demand with much depending on how badly the virus spreads over the course of next week.

Jet fuel demand to fall even further

The coronavirus has now spread into around 80 countries, putting travelers off both business and leisure travel. While in January, only flights in and out of China were being cut, there is now reduced demand for flights along major international routes. Delta and United Airlines have already responded by cutting the number of domestic flights in April and May by about 10% and international flights by 20%. This may end up being a conservative move at this stage.

The bigger problem for the industry is European regulation which requires airlines to continue flying on routes to Europe unless they want to lose their flight spots. This means that airlines are now flying to Europe with close to empty planes, incurring massive costs without any income to compensate for it, a situation that is tenable only for a short period of time as was demonstrated by the collapse of British airline Flybe this week. Look for demand for jet fuel to take a further hit over the coming weeks, particularly from European carriers.

OPEC: What next?

Despite trying to persuade Russia to take part in plans to cut production from OPEC+ countries since mid February, OPEC+ failed to reach an agreement on output cuts Friday. Russia played a round of poker knowing that Saudi Arabia and OPEC will still likely go ahead and reduce output by around 1m bbl to mitigate the coronavirus induced decline in prices. Russia also speculated that it can outlast US producers in surviving a decline in oil prices, which could last for weeks if not months.

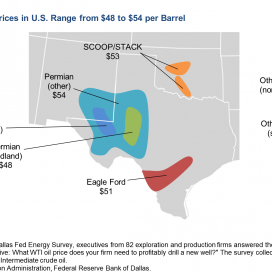

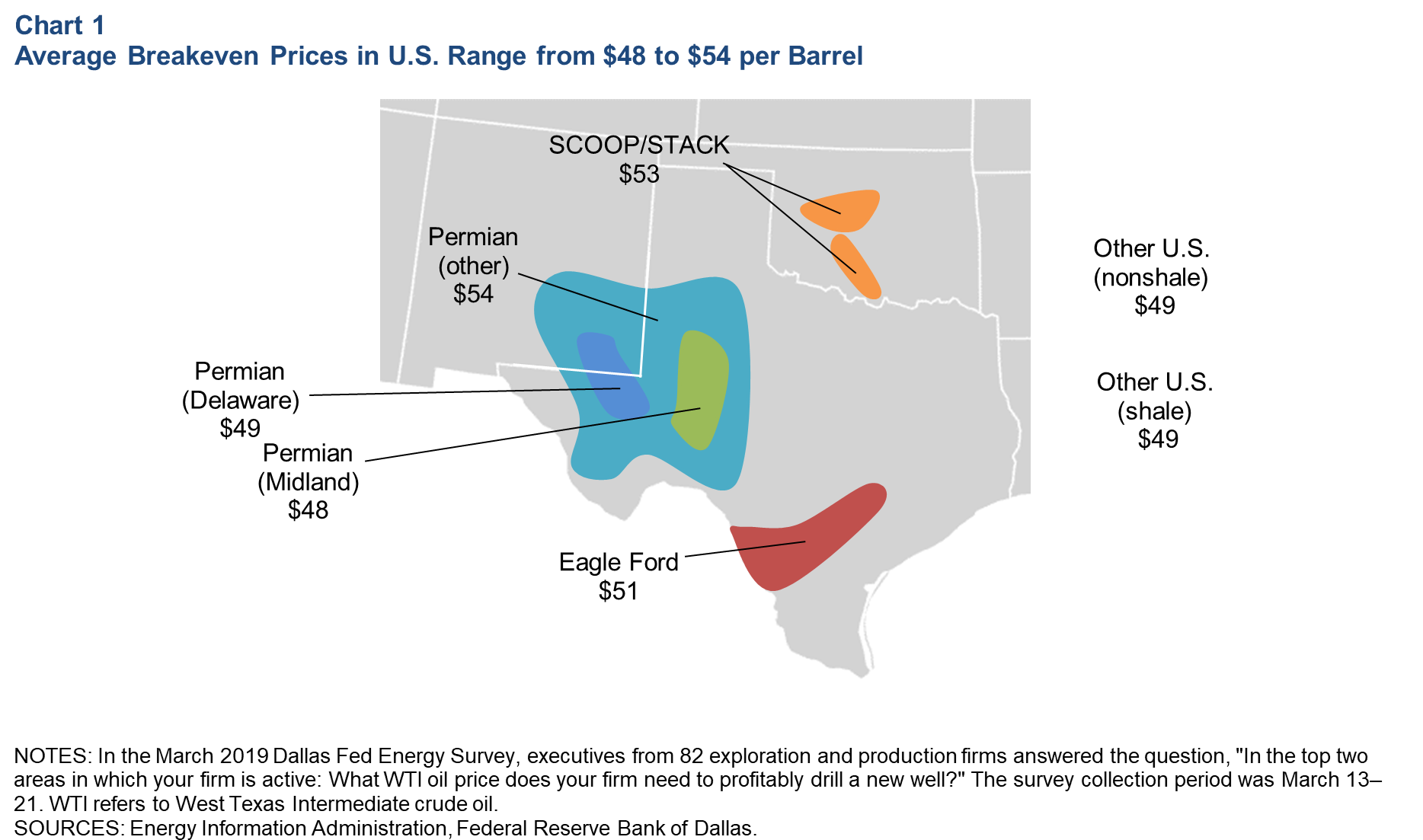

As the picture from the Dallas Federal Reserve below shows, breakeven prices for shale oil production in the US are between $48 and $54 a barrel, depending on the basin. The current prices for WTI of awfully close to $40 will grant smaller US shale oil producers only a short amount of time during which they will be able to continue operating.

Source: Dallas Fed

When

What

Why is it important

Sat 7 March 02.00

China February trade balance

Covers the period when the coronavirus was in full blow in China

Mon 9 March 07.00

Germany industrial production

Y-o-y drop in January was 6.8

Mon 9 March 07.00

Germany Feb trade balance

German exports were close to flat in January. February data will show the hit to exports to China

Tue 10 March 10.00

EU Q4 GDP

Last at 0.1 but the Q4 number may prove less relevant than usual given the spread of COVID-19

Tue 10 March 20.30

API US crude oil stocks

Will show if US stocks are building up and if domestic demand is slowing down

Wed 11 March

OPEC monthly oil report

Updates on production levels in OPEC countries

Wed 11 March 14.30

EIA US crude oil stocks

As above. Last up 0.785m bbl.

Thur 12 March 10.00

EU industrial production

Was down 4.1% in January

Friday 13 March 20.30

CFTC COT oil positions

Weekly change in money managers’ oil positions

Friday 13 March 18.00

Baker Hughes US rig count

Weekly change in number of operational US rigs

Original from: www.forex.com

No Comments on “OIL MARKET WEEK AHEAD: Worse Before it Gets Better”

The site administration is not responsible for the reviews and comments that users wrote.

Newsletter